Unexpected car repairs can strain any household budget, leading many Raleigh drivers of Chevrolet Silverado, GMC Sierra, and Chevy Equinox to seek financing options. When a primary borrower has limited credit history or a low credit score, lenders may require a cosigner for auto repair financing in Raleigh NC. While acting as a cosigner can help a friend or family member access needed repairs (like a $4,000 transmission rebuild on a Chevy Traverse), it carries significant legal and financial responsibilities that many people underestimate. At Creech Import, we have witnessed firsthand how cosigner relationships can strengthen – or strain – personal bonds when expectations aren’t clearly established, especially among GM truck owners who rely on their vehicles for work. This guide explains exactly what cosigning entails, the risks you assume, and how to protect yourself while helping someone in need.

Understanding What a Cosigner Actually Does for Auto Repair Loans

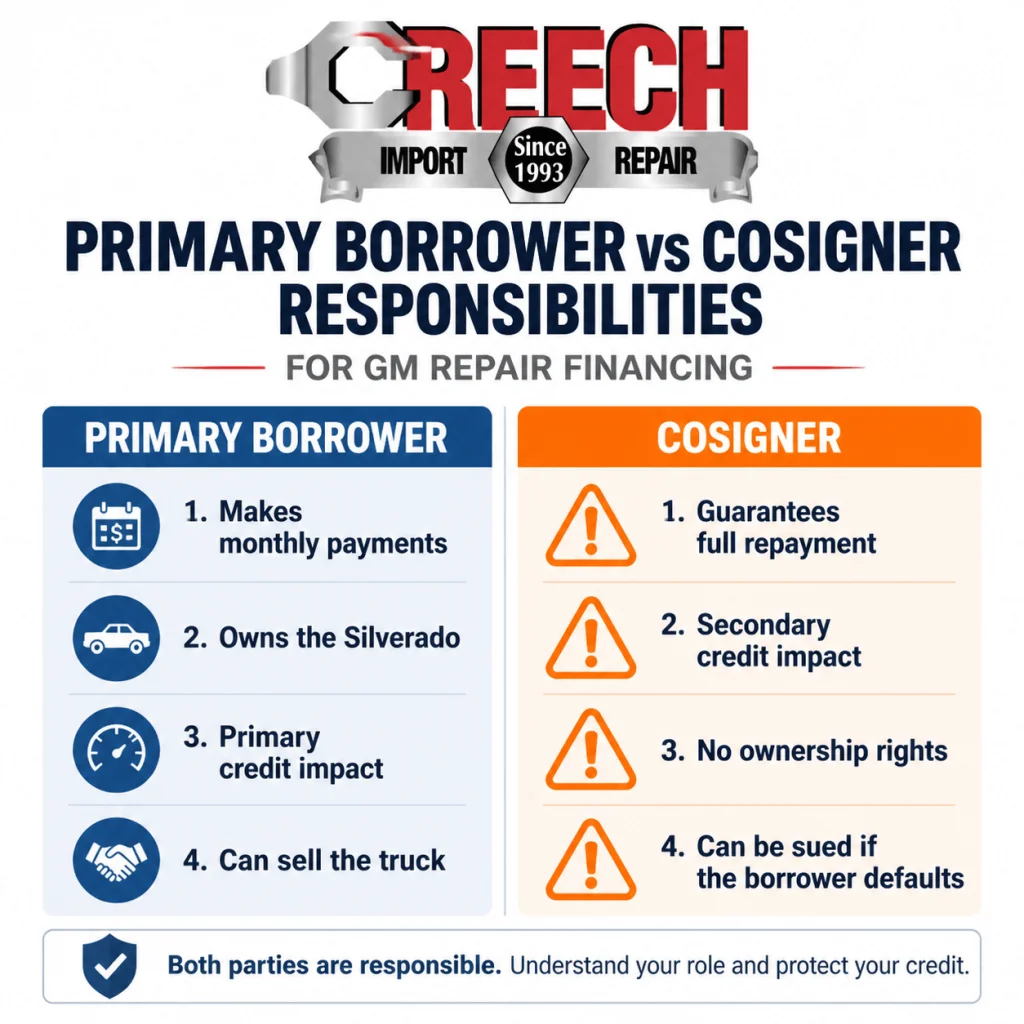

A cosigner agrees to share legal responsibility for a debt alongside the primary borrower. If the primary borrower misses payments or defaults on the loan (e.g., a $3,500 repair loan for a GMC Yukon transmission), the lender can pursue the cosigner for the full remaining balance. Unlike a reference or an emergency contact, a cosigner’s credit report reflects the entire payment history of the loan – every late payment damages both parties’ credit scores.

Key Legal Facts About Cosigning for GM Repair Financing

The cosigner is equally responsible for the entire debt, even if they never drive the vehicle

Lenders can pursue cosigners without first trying to collect from the borrower

Late payments appear on both credit reports – this can affect your ability to finance your own Silverado 2500HD

Cosigners cannot be removed without the primary borrower refinancing (usually impossible if credit hasn’t improved)

Death or bankruptcy of the primary borrower does not release the cosigner

According to North Carolina legal statutes governing auto parts transactions, any person or organization purchasing used motor vehicle parts must maintain proper licensing and records. While this applies to parts dealers, it illustrates North Carolina’s serious approach to vehicle-related financial transactions.

Step 1: Why Auto Repair Financing for GM Trucks Often Requires Cosigners

Major repairs on GM vehicles – such as engine replacement on a Chevy Silverado 1500 with AFM lifter failure (5,000–5,000–8,000), transmission rebuild on a GMC Sierra 2500HD (4,000–4,000–6,000), or hybrid battery replacement on a Chevy Tahoe Hybrid (2,500–2,500–5,000) – can be prohibitively expensive. Many repair shops, including Creech Import, partner with third-party financing companies (Synchrony, Snap-on Finance, etc.) to offer payment plans. These lenders evaluate applicants based on:

Credit score and history (FICO 580+ typically needed for approval)

Income and employment stability

Existing debt obligations (especially auto loans on other GM vehicles)

Payment history on previous loans

Young adults (college students with a Chevy Colorado), recent immigrants, or those rebuilding credit often lack sufficient credit history to qualify alone. A cosigner with stronger credit bridges this gap, potentially securing lower interest rates and better terms.

Step 2: Responsibilities You Assume as a Cosigner for GM Repair Financing

Before signing any document, understand exactly what you are agreeing to. Cosigner responsibilities extend far beyond a simple “I vouch for them” arrangement.

Your Legal Obligations When Cosigning for a Silverado or Equinox Repair

Full repayment liability: You owe the entire remaining balance if the primary borrower stops paying – even if the repair failed or the truck was sold.

Interest accrual responsibility: You are liable for all accrued interest, late fees, and collection costs (APRs on auto repair loans can reach 29.99%).

Credit impact: Every payment (or missed payment) affects your credit score – a default could prevent you from financing your own GMC Sierra.

Legal collection actions: Lenders can sue you, garnish wages, or place liens on your property (including your own GM vehicle).

Bankruptcy limitations: Filing bankruptcy typically does not discharge cosigned debt (the lender can still pursue you).

Research from MIT’s engineering systems division has examined how complex systems with interconnected components can experience cascading failures. Similarly, when a primary borrower’s financial situation unravels, the cosigner is automatically caught in the collapse.

Step 3: Risks Specific to Auto Repair Financing for GM Vehicles

Unlike mortgages or student loans, auto repair financing is often unsecured debt (no collateral beyond the car itself). This structure carries unique risks for cosigners, especially with GM trucks that may have high repair frequency due to known issues (AFM lifter failure, 6L80 transmission problems).

Common Risks for Cosigners of GM Repair Loans

Vehicle depreciation: A 2012 Chevy Suburban with 200k miles may be worth 5,000,buta5,000,buta4,000 transmission repair loan leaves little equity if the borrower wants to sell.

Incomplete repairs: If the borrower stops paying mid-project, you could owe for unfinished work on their Silverado.

Shop quality issues: Poor repairs can lead to repeat failures (e.g., a cheap aftermarket alternator failing again), requiring additional financing.

Total loss scenarios: If the Chevy Traverse is totaled in an accident, insurance may not cover the full loan balance – and you’re still liable.

Before cosigning, verify that the repair shop is reputable. Creech Import has maintained a 5-star rating serving Raleigh GM owners since 1993, providing transparent estimates and quality workmanship using AC Delco and premium aftermarket parts. Choosing a trusted shop reduces the risk of repair-related complications.

Step 4: How to Protect Yourself Before Cosigning for GM Repairs

Taking these precautions can dramatically reduce your risk exposure while still helping someone access needed repairs on their GMC Yukon or Chevy Tahoe.

Pre-Cosigning Checklist for GM Vehicle Financing

Review the borrower’s full financial picture: Income, expenses, other debts (including any existing auto loans)

Discuss realistic repayment ability: Can they truly afford the monthly payment on a $5,000 Silverado repair loan?

Request transparency: Receive copies of all repair estimates (from Creech Import), loan documents, and payment confirmations

Set clear expectations: Agree on what happens if payments become difficult – will they sell the vehicle?

Consider limited cosigning: Some lenders allow “co-borrower” arrangements with defined limits

Check the shop’s reputation: Ensure repairs are necessary and priced fairly – Creech Import provides free second opinions

Questions to Ask the Primary Borrower (GM Owner)

What is your monthly take-home income and total expenses (including existing truck payment)?

Do you have savings for emergencies (at least 3 months of expenses)?

What will you do if you lose your job or face a medical emergency?

Can you set up automatic payments to avoid forgetfulness?

If your Silverado 2500HD needs another major repair in six months, how will you pay for it?

Step 5: Alternatives to Cosigning for GM Repair Financing

If the risks feel too high, several alternatives may achieve the same goal without putting your credit on the line.

Safer Alternatives for Financing Chevy or GMC Repairs

Offer a direct loan: Lend the money yourself with a written promissory note (e.g., $3,000 for their Equinox transmission)

Help with a down payment: Reduce the financed amount so monthly payments are manageable (e.g., put 1,000downona1,000downona4,000 Tahoe repair)

Pay Creech Import directly: Arrange to pay the shop directly for the repairs without involving a financing company

Explore in-house payment plans: Some shops offer their own financing with lower qualification barriers (ask us at Creech Import)

Credit counseling referral: Help the borrower improve their credit for future qualification

At Creech Import, we are happy to discuss payment options and can connect customers with third-party financing partners who offer transparent terms. We also offer our own payment arrangements for repeat customers.

Step 6: What Happens If the Borrower Defaults on a GM Repair Loan

When a primary borrower stops paying (e.g., loses their job and can’t afford the $200/month payment on their Silverado 1500 repair loan), the lender will first attempt collections from them. After 60–90 days of non-payment, however, the lender will contact the cosigner for full repayment.

Default Consequences for Cosigners of GM Repair Financing

Immediate demand for full loan balance (e.g., $3,500 remaining on a GMC Sierra transmission repair)

Negative credit reporting (late payments, charge-off, collections – can drop your FICO score by 100+ points)

Collection agency involvement (frequent calls, letters)

Lawsuit and potential wage garnishment (North Carolina allows garnishment for certain debts)

Difficulty obtaining your own future loans (mortgage, auto loan for your own Chevy Colorado, credit cards)

According to North Carolina legal codes regarding motor vehicle parts transactions, accurate record-keeping and bill of sale requirements protect all parties in financial exchanges. Similarly, keeping meticulous documentation of your cosigned loan protects your interests.

Step 7: How to Exit a Cosigner Agreement for GM Vehicle Repairs

Once you cosign, you cannot simply change your mind. The only ways to remove yourself are:

Full loan payoff: The borrower repays the entire balance (e.g., $4,000 for their Chevy Traverse engine repair)

Refinancing: The borrower qualifies for a new loan in their name only (rarely possible if credit hasn’t improved)

Loan modification agreement: The lender agrees to release you (extremely rare)

Before cosigning, assume you will remain responsible for the entire loan term. If that prospect makes you uncomfortable, explore alternatives.

Why Raleigh GM Owners Should Choose Creech Import for Repair Financing

At Creech Import, we prioritize transparency in all financial discussions. Our service advisors explain repair options clearly (OEM vs aftermarket for your Silverado), provide written estimates, and can connect you with reputable third-party financing partners like Synchrony. We never pressure customers into unnecessary repairs or unfavorable financing terms. We also offer a free second opinion on previous estimates – especially important for GM trucks with known AFM or transmission issues.

Considering cosigning for auto repair financing in Raleigh NC for a Chevy Silverado, GMC Sierra, or any GM vehicle? Make sure the repairs are necessary and fairly priced first. Call Creech Import at 919-872-1999 for a free repair estimate before signing any financing agreement. Visit us at 1818 St. Albans Dr #106, Raleigh, NC 27609 or schedule online.

FAQs

Does cosigning for auto repair financing on my friend’s Silverado hurt my credit score?

The act of cosigning itself doesn’t hurt, but any late payments or default will damage both your and the borrower’s credit.

Can I be removed as a cosigner after the borrower improves their credit?

Only if the borrower refinances the loan in their name alone – which requires qualifying independently with good credit.

What happens if the primary borrower of a GMC Sierra repair loan dies?

As cosigner, you become fully responsible for the remaining loan balance.

Does Creech Import offer in-house financing without a cosigner for Chevy Equinox repairs?

We partner with third-party financing companies; approval decisions, including cosigner requirements, are made by the lender.

How long does auto repair financing typically last for a Chevy Tahoe?

Loan terms range from 6 to 36 months depending on the repair amount and lender.

Can I cosign if I have fair credit (FICO 640)?

Most lenders prefer cosigners with good to excellent credit (680+); poor credit may not help the borrower qualify.

What interest rates apply to auto repair financing for a Silverado 2500HD?

Rates vary from 0% promotional offers to 29.99% APR based on creditworthiness and lender.

Does the cosigner have any ownership rights in the GM vehicle?

No, cosigners have no ownership rights – only financial liability.

What should I do if the borrower misses a payment on their Chevy Traverse repair loan?

Contact them immediately to arrange payment; if needed, make the payment yourself to protect your credit.

How do I know if a repair shop’s estimate for my GMC Yukon is fair?

Creech Import provides transparent, detailed estimates – compare with other local shops or check our 5-star GM customer reviews.

Sources

Why Choose Creech Import Repair for Your Vehicle?

Serving Raleigh since 1993 – Family‑owned, deeply rooted in the community.

✓ ASE‑Certified Technicians – Trained on domestic and import vehicles.

✓ Both domestic and import expertise – One trusted shop for mixed garages.

✓ Transparent pricing & electronic approvals – No surprises, no unnecessary work.

✓ Professional‑grade diagnostic equipment – Advanced scanners and live data analysis.

✓ High‑quality parts & long‑lasting repairs – We don’t cut corners.

📞 Schedule Your Service Appointment Today

Don’t wait until a small problem becomes a major repair. Whether you need routine maintenance, diagnostics, or major repairs, the team at Creech Import Repair is ready to help.

📍 Address: 1818 St. Albans Dr #106, Raleigh, NC 27609

📞 Phone: 919-872-1999

🌐 Schedule Online

About the Author: The ASE‑certified team at Creech Import Repair has been serving Raleigh drivers since 1993. We specialize in both domestic and import vehicles, with extensive experience in repair and maintenance.

Last updated: May 2026. Repair costs are estimates and may vary. Always obtain a written estimate before authorizing repairs.